Real estate taxes in Belgium in 2026: what property ownership really costs

Tax

By: Evi Moors

14 Jul 2026 7 min read

The annual construction holiday is well underway, traditionally the time of year when many Belgians reflect on their housing plans, whether that means renovating, buying or investing. One thing, however, remains unchanged: Belgians have a longstanding passion for real estate.

Property continues to be one of the most popular investment choices. Yet behind the appeal of bricks and mortar lies a less visible reality: taxation.

The tax implications of owning property go far beyond the initial purchase. Taxes may arise throughout the ownership period and again when the property is eventually sold, gifted or inherited.

In this article, we provide a practical overview of Belgian real estate taxation for individuals who hold property in their own name.

Setting the scene: three layers of taxation

When buying and owning real estate in Belgium, individuals are generally confronted with three key tax layers:

- At the time of purchase (registration duties or VAT);

- During the ownership period (property tax and, in certain cases, personal income tax);

- Upon transfer (capital gains tax, gift tax or inheritance tax).

We will look at each of these stages below.

As transaction taxes and transfer taxes are largely regional matters, the rules applicable in Flanders, Brussels and Wallonia do not always align.

Taxes on acquisition: registration duties versus VAT

The first – and often most significant – tax cost arises when acquiring the property. In Belgium, these taxes are determined at regional level, meaning that Flanders, Brussels and Wallonia each apply their own rates and conditions.

When purchasing an existing property, registration duties (also referred to as transfer taxes) are generally due. The purchase of a newly built property, however, may be subject to VAT, particularly where the transaction falls within the VAT regime.

As a rule, the purchase of a new building is subject to VAT at the standard rate of 21%. A building (or part of a building) is considered "new" until 31 December of the second year following the year in which it was first occupied or brought into use.

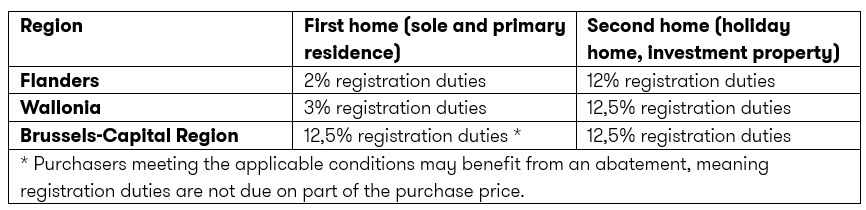

The difference can be particularly significant in Flanders. A buyer purchasing their sole and primary residence benefits from a reduced registration duty rate of 2%, whereas a second home or investment property is subject to a rate of 12%.

Since 2026, the conditions attached to this reduced rate have become more restrictive. Strict requirements now apply regarding the status of the purchaser, the nature of the acquisition and the occupancy obligation. As a result, certain acquisition structures may no longer qualify for the preferential regime.

For example, the purchase must be made by natural persons. This means that the benefit is lost where a company is involved in the acquisition. In addition, the purchase must concern full ownership, which excludes certain structures, such as split acquisitions, from the reduced-rate regime in many cases. Purchasers must also comply with a residency condition by registering their domicile at the property address within the prescribed period and maintaining their residence there for a minimum duration.

In Brussels, the standard rate remains 12.5%. However, qualifying purchasers may benefit from a substantial registration duty exemption (abatement). Under this system, no registration duties are levied on an initial portion of the purchase price, potentially generating savings of up to approximately EUR 25,000, depending on the circumstances.

Wallonia has recently introduced a major reform. A favourable registration duty rate of 3% now applies to a sole and primary residence, provided certain strict conditions are met.

Annual taxes: two tax systems applied to the same property

Once the property has been acquired, annual taxation comes into play. Individuals may be subject to two separate taxes, at least where the property is not their primary residence:

- Property tax, calculated on the basis of the indexed cadastral income; and

- Personal income tax on real estate income, which is often determined based on the indexed cadastral income, except where the property is used for professional purposes, in which case taxation is more closely linked to actual rental income.

Although these are two distinct taxes, they are both built around the same concept: cadastral income.

Cadastral income: not a tax, but a benchmark

Cadastral income is probably one of the most misunderstood concepts in Belgian real estate taxation.

It is not a tax, nor is it intended to reflect the actual rental value of a property. Rather, it is a notional value assigned by the authorities, corresponding to a theoretical annual net rental income based on historical property values dating back to 1975.

This figure serves as the basis for calculating both property tax and personal income tax on real estate income.

Property tax: a tax on ownership

Property tax is an annual levy imposed on ownership rights in real estate. It is payable by whoever is the owner, possessor, long-term leaseholder, holder of a building right or usufructuary of the property on 1 January of the relevant year.

The tax is calculated on the indexed cadastral income.

Provincial and municipal surcharges are added to the base tax, meaning that the final tax burden can vary significantly from one municipality to another. Two identical properties may therefore attract different property tax liabilities simply because they are located in different areas.

Importantly, this tax is entirely separate from income taxation. It is levied solely because the taxpayer owns the property.

Personal income tax: taxation of real estate income

In addition to property tax, real estate income may also be subject to personal income tax.

Here, it is not the property itself that is taxed, but rather the income that the property generates – or is deemed to generate. Once again, cadastral income plays a central role.

For an individual's primary residence, there is generally no longer any taxable real estate income for personal income tax purposes. In practice, only property tax remains due.

For other properties, such as second homes or rental properties, different rules apply. In these cases, a taxable real estate income is calculated, often based on cadastral income.

Rental property: why the property's use matters

The way rental income is taxed depends largely on how the property is used.

When a property is rented to an individual who uses it exclusively for private purposes, or when the property is kept as a second residence, taxation is not based on the actual rent received. Instead, the tax authorities start from the cadastral income, which is indexed and then increased by 40%.

The difference can be substantial.

Assume that you receive annual rent of EUR 12,000 from a property with a cadastral income of EUR 1,750. For income year 2025, the taxable real estate income would be:

EUR 1,750 × 2.2446 × 1.40 = EUR 5,499.27

The factor 2.2446 is the indexation coefficient applicable to income year 2025. As this coefficient is adjusted annually, it may vary from year to year.

In this example, despite receiving EUR 12,000 in annual rent, you would only be taxed on a deemed income of approximately EUR 5,500. As a result, the tax treatment of private residential rentals is often relatively favourable.

The picture changes when the tenant uses the property wholly or partly for professional purposes, for example as an office, medical practice or commercial premises.

In such cases, taxation is generally no longer based primarily on cadastral income. Instead, it more closely reflects the actual rental income and rental benefits received, after application of the legally limited expense deduction.

The consequence is clear: two identical apartments may generate completely different after-tax returns depending solely on the tenant's profile and the use made of the property.

Finally: the end of the property's lifecycle

For the sake of completeness, it is worth noting that the final stage of property ownership may also trigger tax consequences.

Upon a future sale, a taxable capital gain may arise in certain situations, particularly where an individual disposes of the property within a relatively short period after acquisition. The applicable rules depend on the nature of the property, the holding period and the specific circumstances of the transaction. Different rules apply to buildings and land, and each case requires a detailed assessment based on the relevant tax provisions.

Real estate may also be transferred through a gift or inheritance. In such cases, gift tax or inheritance tax may become due.

Not only the applicable rates, but also exemptions, reductions and compliance requirements differ between the Belgian regions and can have a significant impact on the ultimate transfer of wealth.

Conclusion

The tax implications of real estate ownership extend far beyond the purchase price. Depending on the region, the type of property and how it is used, taxes may arise at the time of acquisition, throughout the ownership period and upon transfer.

Anyone buying or holding real estate should therefore consider the full tax picture to avoid unexpected costs and make informed decisions.

A sound understanding of the applicable tax rules can make the difference between a decision that simply feels right and one that is both financially and fiscally well-founded.

At Grant Thornton, we are happy to help you assess the tax implications of your real estate project and provide guidance on your specific real estate tax questions, enabling you to make informed decisions with confidence.