Doing more with less. But at what cost?

International Business Report (IBR)

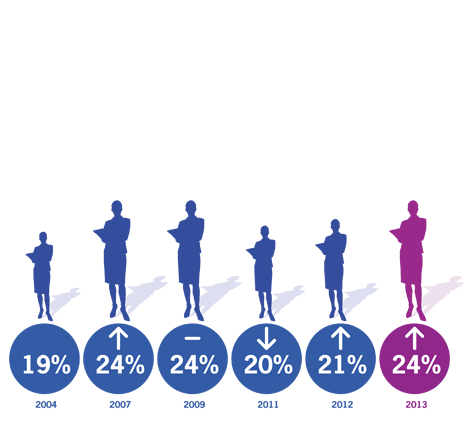

Business leaders in the hospitality & tourism sector are continuing to do ‘more with less’ according to the Grant Thornton International Business Report (IBR) Q3 results. Expectations for business growth remain robust, but job creation is fairly stagnant, reflecting a broader drive for efficiencies within the sector.